If you’ve been selling on Amazon for a while and your business is doing well, it is possible that you have at some point received an offer from Amazon for a small business loan. If you need some extra cash to grow your business, you might be wondering — is a loan from Amazon a good option?

What is Amazon Lending?

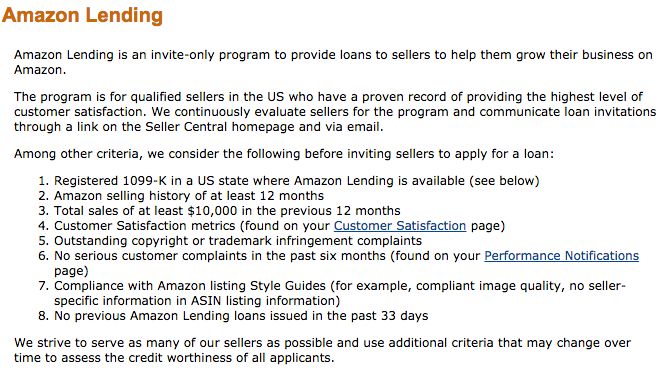

In 2012 Amazon started their small business loan program as a way to support the third party sellers on their site and grow available inventory for their customers. It can be very challenging for a small business to secure a business loan, and the application process is typically pretty tedious, complicated, and lengthy. Also, businesses that don’t operate in a traditional brick and mortar fashion can struggle to meet the collateral requirements that most traditional banks require. So, it isn’t surprising that many small businesses are taking advantage of Amazon’s lending program — Amazon has lent over $1 billion to small business in the last 12 months alone. Over 20,000 small businesses have accepted a loan from Amazon, and over half of those companies have taken out more than one loan from Amazon.

How Amazon Lending Works

Unlike a traditional small business loan, sellers do not apply for a loan from Amazon. Instead, Amazon proactively pre-selects specific third party sellers based on a set of criteria, using sales volume and history as well as other basic performance metrics to identify companies that present a relatively low loan risk. Then Amazon creates a loan offer for a specific dollar amount and notifies the company directly. While the amount included in the loan offer is the maximum a company can borrow, they can also opt to borrow an amount lower than what they were approved for.

The funds loaned by Amazon can be used for one purpose only — purchasing inventory to sell in the Amazon marketplace. Loan amounts range from $1K all the way up to $750K. These are short term loans, with repayment terms of around four to six months. Amazon hasn’t published any specifics on the APR they offer, but various sources around the web have reported offers with rates ranging from 6–18%, which makes them competitive with or better than the interest rates offered by other lending institutions.

The Benefits to Amazon

Sellers are not the only ones who benefit from Amazon lending — Amazon sees some pretty great perks thanks to their lending program, ultimately in the form of increased inventory available for customers to purchase on their site. Because Amazon has access to seller performance data, they can easily identify which sellers are at a low risk of defaulting on a loan. This allows Amazon to make targeted investments in small businesses that are doing particularly well and have the potential to continue growing. As these top performing small businesses grow (with help from Amazon), the stability of Amazon’s third party marketplace grows as well. Not to mention the fact that Amazon makes money on the interest on these loans.

The Pros of Amazon Lending

In addition to the influx of cash a loan from Amazon provides, there are many benefits to taking out a loan from Amazon. Here are just a few:

The Application Process is a Breeze

Instead of spending hours of time filling out complicated paperwork and waiting on your bank to make an approval decision, with a loan from Amazon they do all the hard work for you. Once Amazon identifies your business as a good candidate for a loan and sends you an offer, you are in. All you have to do is accept the offer.

Amazon Offers Competitive Interest Rates

Compared to credit cards and many other small business loan interest rates, the rates offered by Amazon are competitive and in many cases lower than what you can find elsewhere.

An Option When Others Fail

Small businesses selling on Amazon are often either too small to qualify for a traditional bank loan or don’t fit the rigid mold that banks require for granting small business loan approval. And alternative lending options for small businesses often carry risks and expenses that make them less attractive for many small businesses.

The Cons of Amazon Lending

In addition to the benefits that come with a loan from Amazon there are some risks to carefully consider, including these big ones:

Increased Dependency on Amazon

If you are considering taking Amazon up on their loan offer, you need to think about how this plays into any goals you have for business diversification. Since the money you borrow through this program can only be used to purchase inventory that will be sold in the Amazon marketplace, if you choose to borrow money from Amazon you will be growing not just your business, but specifically your business with Amazon. For some sellers this presents zero issue, but for businesses looking to spread their wings beyond the Amazon marketplace this increased dependency on Amazon might not be the right move.

Fixed Payments are Risky

With a small business loan from Amazon, the payments are for a fixed amount that is automatically withdrawn from your Seller Central account. If you have a month of slower than normal sales or the strategy behind your inventory investment doesn’t pan out, you are still on the hook for these payments. If you aren’t able to make your loan payments to Amazon it can mean some nasty consequences for your business. Amazon can hold on to your inventory and restrict sales until you pay them back, or eventually take a more extreme approach of seizing your inventory to sell it and recoup the money you owe them.

Other Sources of Cash for Your Business

While it is often hard for small businesses to qualify for traditional small business loans offered by banks, Amazon lending is not the only alternative option out there. As you weigh out the pros and cons of a loan from Amazon, keep in mind these other options for small business loans:

Online Loan Services

Online loan services (such as Kabbage and UpFund.io) offer a wider range of options to Amazon sellers who don’t qualify for traditional small business loans. But as with any loan, you need to read the fine print carefully and consider the interest rate and various fees to decide if a loan like this make sense for your business. Here is a brief overview of both of these services to help you can weigh the pros and cons of each:

Kabbage

How it Works

Kabbage offers small businesses a line of credit of up to $150,000. Kabbage makes loan decisions based on the health of your business as well as your credit score. As your business grows, so does your line of credit, without having to submit a new application every time you want to access funds. The application process is free, with no obligation to accept funds. You can accept any increment of funds from your line of credit as often as once every 24 hours. Funds can either be direct deposited to your account, or you can use the Kabbage Card to make purchases directly.

Kabbage offers small businesses a line of credit of up to $150,000. Kabbage makes loan decisions based on the health of your business as well as your credit score. As your business grows, so does your line of credit, without having to submit a new application every time you want to access funds. The application process is free, with no obligation to accept funds. You can accept any increment of funds from your line of credit as often as once every 24 hours. Funds can either be direct deposited to your account, or you can use the Kabbage Card to make purchases directly.

Fees

Instead of an APR, Kabbage uses a flat fee of 1.5–10% of the loan amount.

Term

Kabbage offers the option of either a 6- or 12-month repayment term.

Payment

Payments are automatically deducted from your bank account each month, in equal increments (either 1/6th or 1/12th of the amount owed, based on the loan term), plus the flat monthly fee.

Pros

Super simple terms, free and fast application with no obligation to accept funds, business size and health as well as credit history determine approval, easy to access funds, and no prepayment penalty—if you pay off the loan early you can save big on fees.

Cons

Minimum qualification requirements (at least one year in business, with a business revenue of at least $50,000 annually or $4,200 per month for the last three months) make this option unattainable for smaller or newer Amazon businesses. No consideration of lead and shipping times for repayment schedule.

UpFund.io

How it works

UpFund.io is an inventory funding loan service specifically for Amazon sellers. Loan decisions are made based on your Amazon sales history and business performance as well as your credit history. Once you receive loan approval, funds are direct deposited into your bank account. For your first loan request you can receive funds of anywhere from $2,000 to $75,000. There is no obligation to accept funds upon application.

UpFund.io is an inventory funding loan service specifically for Amazon sellers. Loan decisions are made based on your Amazon sales history and business performance as well as your credit history. Once you receive loan approval, funds are direct deposited into your bank account. For your first loan request you can receive funds of anywhere from $2,000 to $75,000. There is no obligation to accept funds upon application.

Fees

Instead of an APR, UpFund.io uses a flat fee ranging from 6–15% of the loan amount.

Term

The term of the loan is based on the lead and shipping time you select, but once payments begin you will make four payments over a period of two months. For example, if you indicate a 60 day lead and shipping time, your first payment is due on the 60th day, and the next three payments are due every 15 days thereafter.

Payment

The repayment amount is based on a scaling percentage of the principal owed, as well as an Annual Percentage Yield (APY)—so, not exactly an easy-to-calculate figure. UpFund.io defines the APY as how long it takes to return the money and how much it earns in that time, extrapolated over a year. You can find examples of this calculation in their FAQ’s, but in a nutshell, you can expect to see payment amounts that increase over the term of the loan.

Pros

Payment schedule accounts for lead and shipping time, free and fast application with no obligation to accept funds, and business size and health as well as credit history determine approval.

Cons

Complicated repayment schedule and amounts due at each payment make this a bit tricky to understand and plan for. Loans are limited to inventory purchases for one parent ASIN per loan, so if you plan to purchase inventory for additional ASINs you will need to apply separately for each ASIN. Unclear how — or if — prepayment could result in lower fees.

SBA Microloans

The Small Business Association (SBA) has a microloan program that can be a good option for some small businesses. These loans are specifically for amounts of up to $50,000 with the average SBA microloan being around $13,000. Microloans are funded with government dollars and the terms, interest rates, and eligibility requirements are all determined at a local level. Interest rates generally range from 8–13%, and the maximum repayment term is 6 years. You can apply for this type of loan by working with an SBA approved intermediary in your local area.

Peer to Peer (P2P) Lending

Another way to raise some extra cash for your Amazon business is to visit a peer to peer (P2P) lending site (such as Lending Club, Upstart, Prosper, or Funding Circle). With these sites, you can specify what interest rate you want to pay and potential lenders will then bid on your loan. You do need to have good personal credit to utilize these services, so keep that in mind.

Credit Cards

While high interest rates make this option potentially less attractive than others, in a pinch a credit card can be a helpful option. It is generally best to use this option when you know you can pay off the balance relatively quickly, depending on your interest rate and other fees. If you have particularly good credit you may be able to take advantage of the occasional promotional offer from certain credit card companies providing a lower-than-normal interest rate at a limited term.

Home Equity Line of Credit (HELOC)

If you own your home and have at least 20–30% equity, a HELOC is another option for gaining access to cash for your Amazon business. You can typically borrow up to 80–90% of your home equity, with around a 3–8% APR. The low rates on this option are a big plus, but keep in mind the risks — you could lose your house if you can’t pay back the loan.

Is a Loan from Amazon Right For You?

So, with all of this in mind, how do you decide if you should take Amazon up on their loan offer? While this is a decision that will vary greatly from business to business, there are a few basic questions you can ask yourself that will go a long way in helping you make an informed decision:

How confident are you in your sales growth strategy?

With the risks that come with a fixed and automatic repayment to Amazon, you need to be confident that you can pay back your loan. Before you take out a loan from Amazon you need to have a solid strategy in place to grow your sales—maybe increasing your outside marketing efforts or creating Sponsored Products Campaigns for your listings. Optimizing your listings to improve sales conversions is another great sales growth strategy.

Grow Sales By Increasing Customer Reviews

One of the best ways to increase sales is by increasing the number of customer reviews for your products. With Salesbacker you can automatically send an email to every customer who purchases your products, politely asking them to provide feedback in the form of a customer review. Sign up for your free 30-day trial of Salesbacker to start growing the number of customer reviews for your products today.

What are your goals for business diversification?

If your main business growth goal is to grow your business outside of the Amazon marketplace then a loan from Amazon is probably not a great choice, unless you are simultaneously investing in your other sales streams.

What other options—if any—are available to you, and how do the rates, fees, and terms compare?

While Amazon offers competitive loan rates and fees, depending on your particular situation there may be a loan out there that just makes better financial sense for your business. Be sure you’ve done your homework so you can be confident you are getting the best deal out there.